Common Errors in Personal Financial Planning and How to Avoid Them

Understanding Financial Planning Mistakes

In an era where financial literacy is more crucial than ever, many still find themselves entangled in financial uncertainty due to avoidable mistakes. Making informed financial decisions can significantly influence an individual’s capability to secure a comfortable future. Recognizing common pitfalls is the first step in transforming financial aspirations into a tangible reality.

Neglecting to Create a Budget

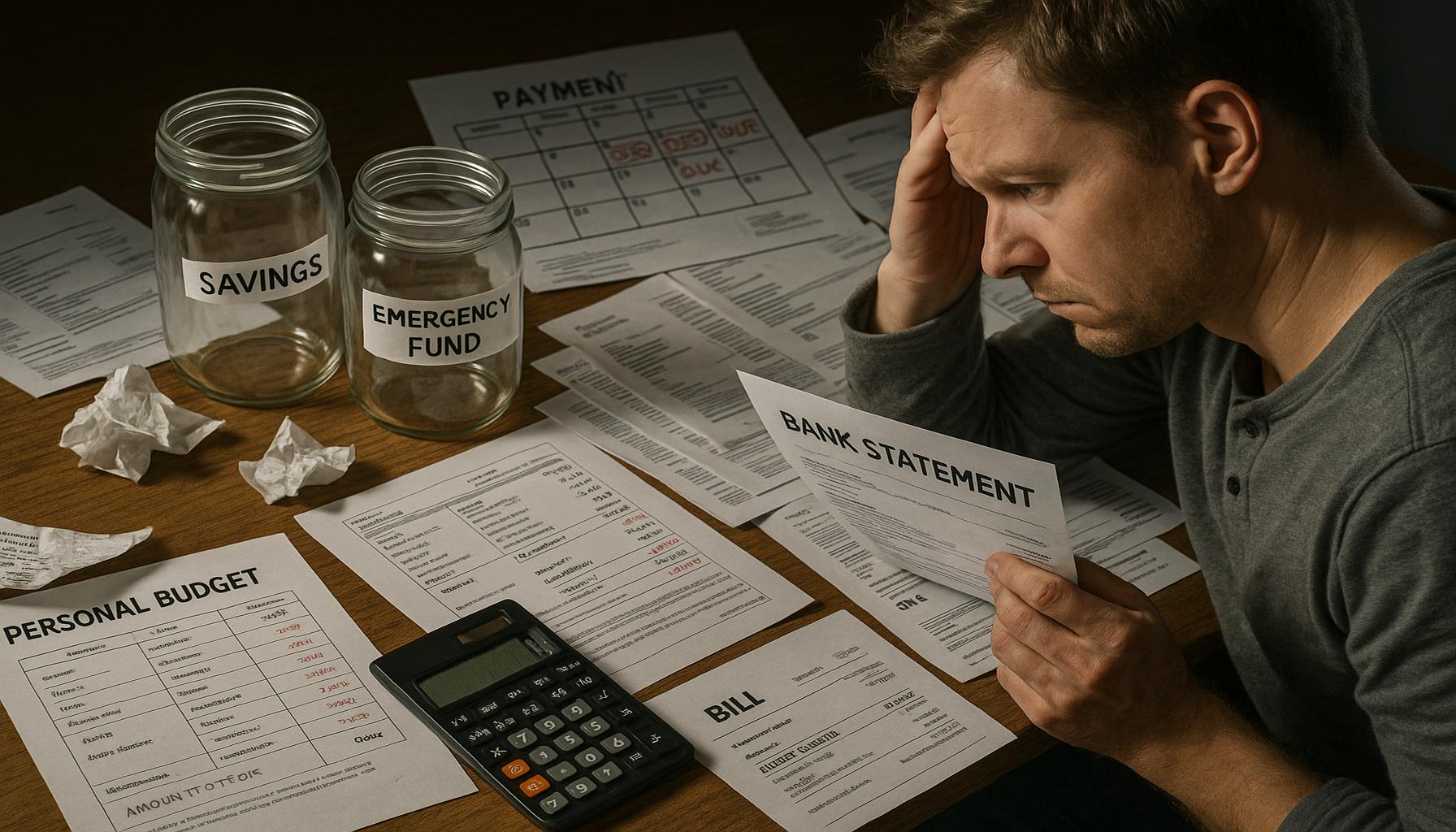

One of the most prevalent mistakes people make is neglecting to create a budget. A budget acts as a roadmap for your finances; without it, expenses can spiral dangerously out of control. For instance, many individuals may underestimate their monthly spending on dining out or subscription services, leading to an unexpected financial shortfall. According to a survey by the National Endowment for Financial Education, nearly 60% of Americans do not operate on a budget.

To combat this issue, individuals should start by tracking their income and expenditures. Creating a simple spreadsheet or using budgeting apps can help visualize cash flow. This approach not only ensures that bills are paid on time but also promotes a habit of saving, which is essential for future investments.

Ignoring Debt Management

Another critical error is ignoring debt management. Many consumers juggle multiple debts, including credit cards and loans, often focusing solely on minimum payments. This strategy can lead to a quagmire of high-interest charges, prolonging financial recovery and leading to increased stress. According to Experian, the average American carries over $5,000 in credit card debt, which compounds rapidly if not managed properly.

To address this challenge, individuals should develop a plan to tackle debt systematically. Consider the snowball method, where one focuses on paying off the smallest debts first, which can foster a sense of accomplishment and motivate further repayments. Alternatively, the avalanche method prioritizes debts with the highest interest rates, ultimately saving money over time.

Underestimating the Importance of an Emergency Fund

Lastly, underestimating the importance of an emergency fund is another financial misstep that can leave individuals vulnerable to financial shocks. Unexpected expenses, such as medical emergencies or car repairs, can arise without warning. A common rule of thumb is to have three to six months’ worth of living expenses saved. However, many Americans struggle to have even a small cushion set aside.

Establishing an emergency fund doesn’t happen overnight, but small, consistent contributions can build resilience over time. Consider setting up an automatic transfer to a savings account designated for emergencies. Such practice not only prepares individuals for uncertainty but also fosters a greater sense of financial security.

By becoming aware of these frequent financial mistakes, individuals can make significant strides toward improved financial health. Through diligent budgeting, effective debt management, and committed savings towards an emergency fund, one can pave the way for financial independence. As the adage goes, “A goal without a plan is just a wish.” Recognizing potential pitfalls and actively mitigating them is essential for achieving financial stability and success.

DON’T MISS: Click here for essential financial tips

Avoiding Common Financial Planning Pitfalls

Achieving financial success is often a complex journey, and navigating through it can become challenging without a clear strategy. Individuals frequently stumble over common errors that hinder their financial growth. By identifying these issues and implementing strategies to avoid them, it becomes possible to build a more secure financial future.

Failing to Set Clear Financial Goals

One overwhelming mistake is failing to set clear financial goals. Many people have aspirations of financial stability or wealth but lack a concrete plan to achieve these ambitions. Without well-defined objectives, such as saving for retirement, purchasing a home, or paying off student loans, it can become easy to lose focus and motivation. According to a study published by the American Psychological Association, having specific goals can increase the likelihood of achieving them by over 40%.

To avoid this pitfall, it’s important to establish SMART goals—those that are Specific, Measurable, Achievable, Relevant, and Time-bound. For instance, instead of a vague desire to “save more,” a clearer goal would be “to save $10,000 for a down payment on a house within the next three years.” Creating written goals not only clarifies your intentions but also provides a track to measure your progress.

Overlooking Retirement Savings

Overlooking retirement savings is another common error that can have dire consequences. Many individuals prioritize immediate financial needs and desires over long-term savings, often believing they have plenty of time to think about retirement. However, the reality is that the earlier one starts saving for retirement, the more they can benefit from compound interest. According to a report from the Economic Policy Institute, roughly 66% of working-age Americans do not have any retirement savings.

To tackle this issue effectively, individuals should begin contributing to retirement accounts as soon as they enter the workforce. Utilizing employer-sponsored plans like a 401(k), especially if there’s a company match, is an excellent way to boost retirement savings. For those who are self-employed or lack access to a workplace retirement plan, options like a Traditional or Roth IRA are viable alternatives to start building a nest egg.

Neglecting Regular Financial Reviews

Many people also make the oversight of neglecting regular financial reviews. It’s easy to set up a financial plan and then forget about it. However, life circumstances change, and so do financial goals; hence, a periodic review is essential to adapt your strategies accordingly. A significant life event, such as marriage, having children, or changing jobs, can impact your financial landscape dramatically.

- Schedule reviews annually: Dedicate time once a year to examine your budget, savings goals, and debt situation.

- Adjust as necessary: Make changes to your financial plan based on shifts in your life circumstances or income.

- Consult a financial professional: If you’re uncertain about your plan, don’t hesitate to seek guidance from a financial advisor who can offer expert advice.

In conclusion, the road to financial stability can be riddled with obstacles, but recognizing and understanding common financial planning errors is key to overcoming them. By setting clear financial goals, prioritizing retirement savings, and conducting regular reviews, individuals can head toward a more motivated and successful financial future. Each of these steps is one that can change the trajectory of your financial journey for the better.

LEARN MORE: Click here for insights on financial vs. estate planning

Recognizing Additional Financial Planning Missteps

As individuals traverse the intricate world of personal finance, various aspects can either facilitate or hinder their financial journey. Beyond the errors already discussed, several other pitfalls can significantly derail financial aspirations. Understanding these can empower individuals to create a more robust and sustainable financial plan.

Ignoring Debt Management

One of the most detrimental mistakes people make is ignoring debt management. While accumulating debt can sometimes be unavoidable due to emergencies or education, allowing it to spiral out of control can create long-term damage to one’s finances. High-interest debt, such as credit card balances, can quickly become overwhelming and impede progress toward financial goals.

To combat this issue, it’s crucial to develop a clear strategy for managing and paying off debt. Techniques like the snowball method, where you focus on paying off the smallest debt first, can provide psychological incentives to remain committed. Additionally, individuals should consider consolidating high-interest debts into a lower-interest loan, allowing them to minimize overall interest payments and pay off their debts faster.

Underestimating Lifestyle Inflation

Underestimating lifestyle inflation is another common error that can lull individuals into a false sense of financial security. As salaries increase or financial circumstances improve, many feel inclined to elevate their standard of living, accumulating unnecessary expenses that can outpace their growth. According to a survey by the Bureau of Labor Statistics, consumer spending tends to rise in tandem with income, emphasizing the importance of mindful spending habits.

To mitigate lifestyle inflation, it’s wise to adopt a lifestyle that does not fully reflect your current earnings. Prioritize saving a percentage of every raise or bonus received. Implementing the “pay yourself first” philosophy, where savings contributions are made before discretionary spending, can ensure ongoing financial health even as income rises.

Neglecting Insurance Protections

Neglecting insurance protections poses a significant risk that can lead to financial chaos. Many individuals overlook the importance of suitable insurance coverage, believing it to be an unnecessary expense. However, the right insurance can be instrumental in safeguarding against unforeseen challenges, including medical emergencies, accidents, and property loss.

- Evaluate your needs: Regularly assess which types of insurance (health, auto, home, life) are essential based on individual circumstances.

- Shop around: Don’t settle for the first policy; exploring multiple options can reveal better coverage at a competitive price.

- Review policies often: As life circumstances change, ensure that insurance coverage remains relevant and sufficient to meet your needs.

Failing to Educate Oneself About Finances

Lastly, a significant obstacle is failing to educate oneself about personal finances. Many individuals shy away from financial literacy, feeling intimidated by complex terms and ideas. This lack of knowledge can lead to uninformed decisions that can harm cumulative wealth over time.

To combat this, dedicating time to learning about financial concepts, investment options, and budgeting techniques is paramount. Various resources, such as online courses, personal finance books, and community workshops, can provide valuable insights. Engaging in discussions with financially savvy friends or even exploring podcasts on finance can enhance one’s understanding and confidence in managing personal finances.

The world of financial planning is filled with potential errors that can impact one’s future. However, by confronting issues such as debt management, lifestyle inflation, insurance protections, and the necessity of financial education, individuals can equip themselves with the knowledge and tools required for effective financial planning. Each small step taken towards rectifying these mistakes can contribute to long-term success and stability.

DISCOVER MORE: Click here to learn how to safeguard your assets

Conclusion

Navigating the complex realm of personal finance is a journey that requires diligence, foresight, and a commitment to continuous improvement. The common errors in personal financial planning can have profound repercussions, impacting one’s ability to achieve financial goals. For instance, failing to manage debt effectively can lead to high-interest burdens that accumulate over time, making it difficult to invest or save for future needs. Similarly, lifestyle inflation—which occurs when spending increases as income rises—can eat away at potential savings, undermining long-term financial stability.

Moreover, neglecting essential insurance protections can leave individuals exposed to unexpected financial downturns. For example, without adequate health insurance, a single medical emergency could lead to crippling debt. On the other hand, a lack of financial education can result in poor investment choices, further complicating one’s financial situation. By identifying and addressing these issues, individuals can significantly enhance their financial well-being.

Additionally, it’s essential to foster a proactive mindset in financial planning. This means not only reacting to existing financial challenges but also anticipating potential setbacks before they materialize. Taking the time to regularly review one’s financial situation, perhaps quarterly or annually, can help in adjusting strategies that align with changing life circumstances and aspirations. Surrounding oneself with a network of financially literate individuals, engaging with financial advisors, or participating in community workshops can provide valuable insights and strategies to navigate personal finance effectively.

Ultimately, the key takeaway is that personal financial planning is not a one-time task but an evolving process. Individuals must continuously assess and adapt their strategies to navigate changing circumstances and economic landscapes. By embracing the principles outlined and understanding the intricacies of financial management, people can lay the groundwork for lasting financial success and stability, ensuring not only their own financial peace of mind but also that of their families for generations to come.

Related posts:

Difference between personal financial planning and estate planning

The Importance of Health Insurance in Personal Financial Planning

How to Create a Sustainable Financial Plan

Financial Planning: Integrating Insurance to Minimize Risks

Financial checklist for those nearing retirement

Financial Planning Strategies for a Comfortable Retirement

Beatriz Johnson is a seasoned financial analyst and writer with a passion for simplifying the complexities of economics and finance. With over a decade of experience in the industry, she specializes in topics like personal finance, investment strategies, and global economic trends. Through her work on our website, Beatriz empowers readers to make informed financial decisions and stay ahead in the ever-changing economic landscape.