How to Deal with Debt and Integrate It into Your Monthly Budget

Understanding the Landscape of Debt in Canada

Managing debt can feel overwhelming, especially when trying to maintain a balanced monthly budget. Many Canadians find themselves juggling multiple debts, including credit cards, student loans, and personal loans. These financial obligations can weigh heavily on one’s mind, often leading to stress and anxiety. The key to achieving financial stability lies in recognizing the impact of these debts and learning to integrate them into a comprehensive budget.

Types of Debt Encountered

Before diving into solutions, it’s essential to understand the different types of debt you may come across:

- Secured debt: This includes loans that are backed by collateral, such as mortgages or car loans. Lenders are more willing to offer lower interest rates on secured debts because they can reclaim the asset if payments are not made.

- Unsecured debt: Unlike secured debts, these loans are not tied to any asset. Common examples are credit cards and medical bills. Since they carry a higher risk for lenders, unsecured debts usually feature higher interest rates.

- Student loans: These are specific to education and often come with various repayment options. In Canada, government-backed student loans may offer flexible repayment plans based on income, allowing graduates to manage their payments effectively while transitioning into the workforce.

Proactive Steps Toward Debt Management

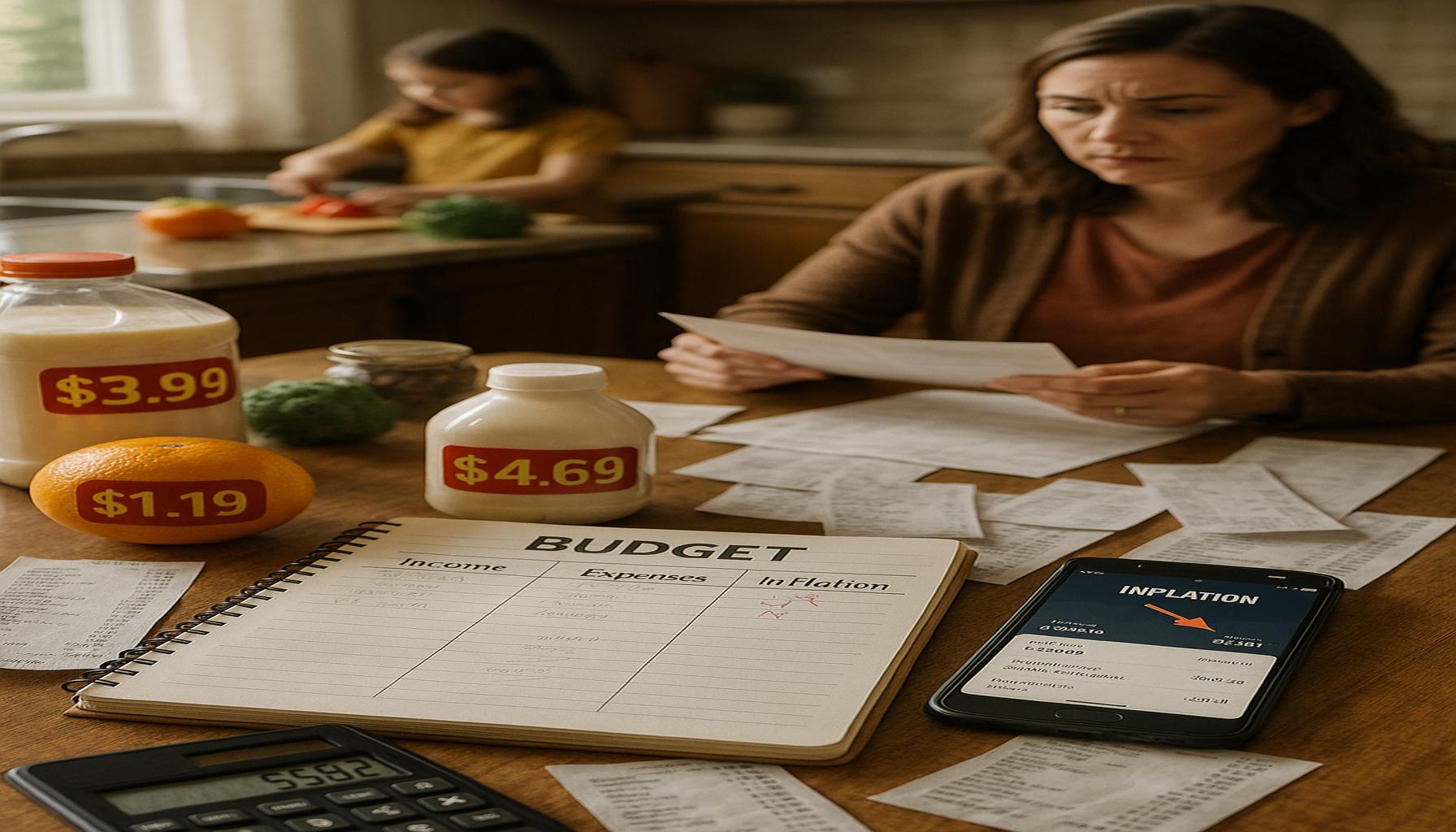

With a clear understanding of your debts, the next step is to take proactive measures for effective management. Start by assessing your total debt in relation to your income. One common approach is to calculate your debt-to-income ratio, which allows you to see how much of your monthly income is consumed by debt payments. This analysis empowers you to create a practical budget that accommodates your financial realities.

When budgeting for debt, consider these crucial elements:

- Track your expenses: Knowing where your money goes is vital. Keeping a detailed record will help identify unnecessary expenditures that can be cut back, freeing up more funds for debt repayment.

- Prioritize payments: If you have multiple debts, focusing on high-interest obligations first can save you a significant amount of money in the long run. For example, paying off a credit card with 20% interest before a personal loan at 8% can minimize your overall interest payments.

- Consider debt consolidation: Merging multiple debts into a single payment can simplify your financial management. Options for consolidation may include a personal loan with a lower interest rate or a balance transfer credit card. In Canada, many credit unions and banks offer competitive rates for such services.

Working Towards Financial Freedom

By integrating these debt management strategies into your budgeting process, you can make significant strides toward achieving financial freedom. Remember, every small step counts in this journey. Being well-informed and proactive about your financial choices is the first step toward alleviating the burden of debt. Whether it’s attending a workshop on financial literacy or seeking the advice of a financial advisor, every action can lead you closer to a more secure financial future.

Ultimately, managing debt is about creating a healthy relationship with your finances. By taking control of your debts, you will be better positioned to fulfill your financial goals, whether that means saving for a home, planning for retirement, or simply enjoying a more stress-free lifestyle.

LEARN MORE: Click here for the full guide

Crafting Your Budget: The Framework for Debt Management

Once you have a solid understanding of the various types of debt you might be facing, the next step is to create a budget that effectively accommodates these financial obligations. A well-structured budget is essential for managing debts and allows you to track not only your income and expenses but also your progress toward becoming debt-free. Building a budget tailored to your needs requires a few foundational steps.

Gather Your Financial Information

The first step in crafting an effective budget is to gather all of your financial information. This includes your income, expenses, and debts. Document your income sources—whether it’s from your job, freelance work, or other avenues—and record them on a monthly basis. Just as importantly, list all your expenses, which can be categorized into fixed and variable:

- Fixed expenses: These are regular, monthly payments that typically remain constant over time, such as rent or mortgage payments, insurance premiums, and loan repayments.

- Variable expenses: These costs fluctuate and can include groceries, entertainment, and transportation expenses. Monitoring these costs allows you to identify areas where you can cut back.

Having all of this information at your fingertips makes it simpler to see where your money goes and how it relates to your obligations. This clarity is crucial for making informed financial decisions.

Set Clear Financial Goals

With a comprehensive view of your finances, the next step is to set specific, measurable, attainable, relevant, and time-bound (SMART) goals related to your debt. Having clear financial objectives helps you stay motivated and focused. For instance, you might aim to pay off a particular credit card by the end of the year, or decrease your student loan balance by a set percentage within six months. When setting these goals, consider the following:

- Short-term goals: Paying off small debts or making premium payments can create a sense of achievement and motivate you to keep going.

- Long-term goals: These can include major milestones such as saving for a home or becoming debt-free in the next few years. Being aware of these goals ensures they remain at the forefront of your financial priorities.

Implementing Your Budget

Once you’ve structured your financial information and set your goals, it’s time to implement your budget. Start by establishing a monthly spending plan that allocates specific amounts to each category, ensuring that a portion of your income goes toward debt repayment. This can be done using various methods, including the traditional envelope system or modern budgeting apps that help track spending in real time.

Furthermore, revisiting your budget on a monthly basis will allow you to adjust as necessary, especially if you experience changes in income or unexpected expenses. The key is to remain flexible while staying committed to your overall financial goals.

Integrating debt management into your budget isn’t just about paying off what you owe; it’s about fostering a healthy relationship with your finances. By taking control of your budgetary framework, you can transform your approach to debt and journey toward a more financially stable future.

DISCOVER MORE: Click here for the details

Prioritizing Debt Repayment Strategies

As you delve deeper into managing your debt within your budget, it’s vital to adopt effective repayment strategies that maximize your financial resources. Understanding the difference between your various debts, and how to prioritize them can significantly impact your journey toward a debt-free life. There are two popular methods recognized in the financial community: the snowball method and the avalanche method.

Snowball Method: Small Wins to Build Momentum

The snowball method encourages you to tackle your smallest debts first. This approach allows you to focus your efforts on paying off low-balance debts quickly. Here’s how it works:

- List your debts from smallest to largest regardless of the interest rates.

- Allocate additional funds toward the smallest debt while making minimum payments on your other debts.

- Once the smallest debt is paid off, redirect the amount you were paying toward that debt to the next smallest one in line.

This method is particularly effective for those who thrive on motivation and accomplishment. By celebrating small victories, you gain the confidence to continue your financial journey. In Canada, where consumer debt can reach significant levels, this method can serve as a powerful psychological tool for individuals feeling overwhelmed by their financial obligations.

Avalanche Method: A Focus on Interest Rates

On the other hand, the avalanche method prioritizes debts with the highest interest rates first. This method might save you the most money in interest paid over time:

- List your debts from highest to lowest interest rate.

- Direct any extra funds toward the debt with the highest interest rate while making minimum payments on others.

- As you pay off higher-interest debts first, you reduce the overall cost of your debt significantly.

For Canadians grappling with high-interest credit card debt, the avalanche method can prove particularly beneficial. It emphasizes long-term savings and helps build a more economical approach to debt reduction.

Utilizing Windfalls and Saving for Emergencies

Integrating debt repayment into your monthly budget also requires adaptable strategies. One way to accelerate debt repayment is by utilizing unexpected financial windfalls, such as work bonuses, tax refunds, or gifts. Instead of spending this unexpected cash, consider applying it directly towards your highest-priority debts. This can drastically shorten your repayment timeline and save you money in interest payments.

Additionally, it’s important to strike a balance between debt repayment and maintaining an emergency fund. Financial experts recommend having at least three to six months’ worth of living expenses saved in an easily accessible account. This does not mean sacrificing all your debt repayments but rather allocating a small portion of your budget toward building that safety net. This can prevent you from accruing additional debt due to unforeseen expenses.

Staying Accountable

Finally, accountability plays a crucial role in successful debt management. Find ways to hold yourself accountable by sharing your goals with a trusted friend or family member. You could also consider joining local financial workshops or online forums where people discuss budgeting and debt repayment strategies. Being part of a community increases your motivation and engagement with your financial journey.

By prioritizing your debt repayment strategy and leveraging your budget effectively, you can navigate your financial obligations with confidence and clarity. The road to becoming debt-free requires discipline and commitment, but by integrating these aspects into your monthly budget, you’ll be well on your way to achieving your financial goals.

DISCOVER MORE: Click here for details

Conclusion: Taking Control of Your Financial Future

In conclusion, tackling debt and effectively integrating it into your monthly budget is a journey that requires both readiness and resilience. By employing methods such as the snowball and avalanche techniques, you can create a tailored repayment strategy that aligns with your financial situation and personal motivations. Understanding your debts and prioritizing them accordingly lays a solid foundation for success.

Moreover, being proactive by utilizing unexpected financial windfalls, while concurrently setting aside emergency savings, ensures that you are prepared for unforeseen circumstances without spiraling back into debt. This balance fosters a sense of security that is essential for thriving financially in Canada’s ever-changing economic landscape.

Remember, accountability is your ally in this endeavor. Engage with trusted friends or participate in community forums; sharing your goals can enhance your commitment and provide vital support. Ultimately, achieving a debt-free life is not merely about numbers—it’s about cultivating a healthier relationship with money, embracing responsibility, and gradually working toward financial freedom.

By adopting these strategies and remaining steadfast in your commitment, you not only address current debts but also pave the way for a more prosperous future. Embrace the journey ahead with confidence, knowing that each step, no matter how small, brings you closer to achieving your financial aspirations.

Linda Carter

Linda Carter is a writer and financial expert specializing in personal finance and financial planning. With extensive experience helping individuals achieve financial stability and make informed decisions, Linda shares her knowledge on our platform. Her goal is to empower readers with practical advice and strategies for financial success.