The Impact of Inflation on Family Budget: Tips to Adjust Your Finances

Understanding Inflation and Its Effects

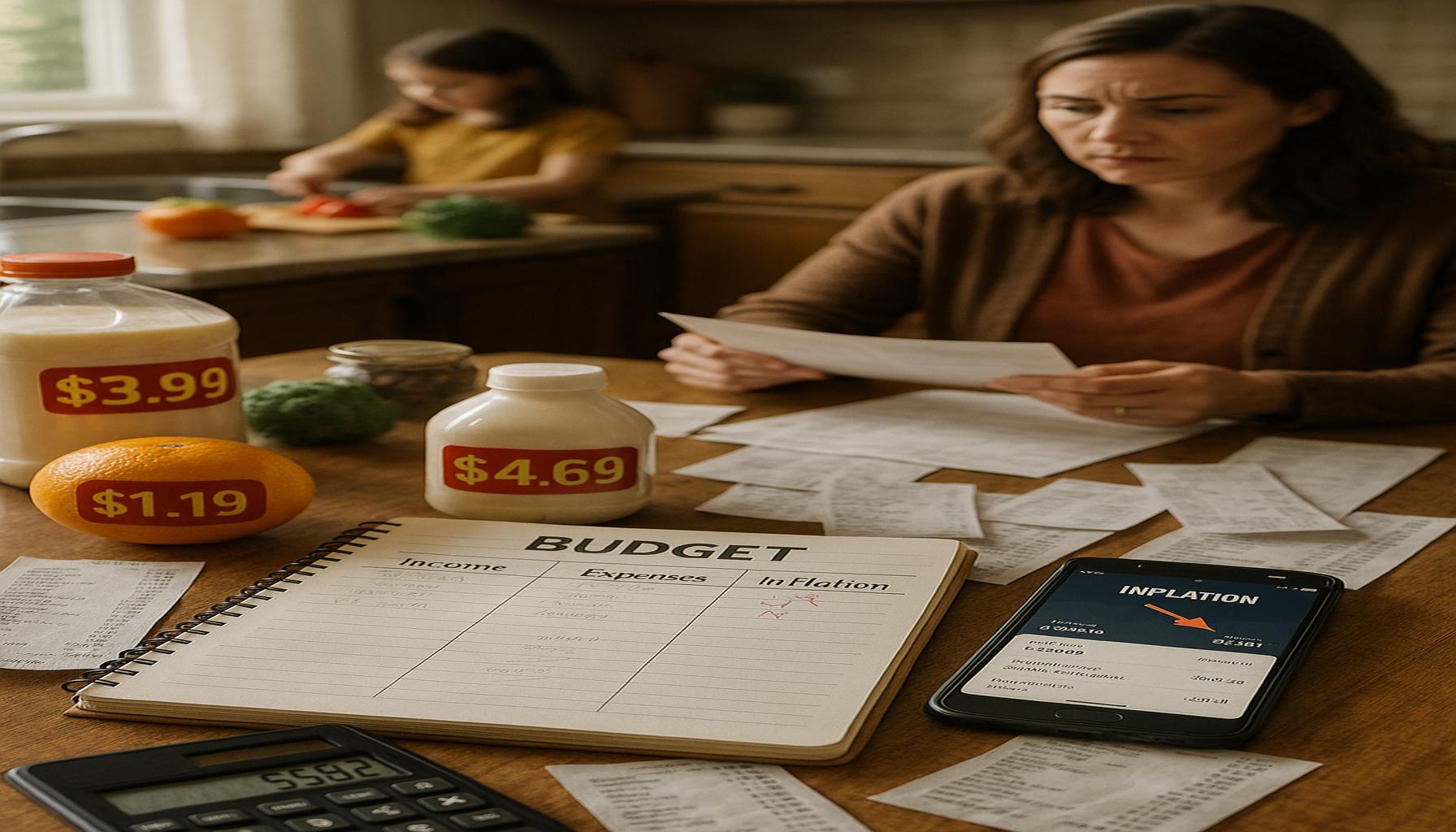

Inflation can feel like a silent thief, quietly eroding the purchasing power of your hard-earned money. As prices for essentials such as food, gas, and housing rise, families across Canada are faced with the challenge of managing tighter budgets. Every month, Canadians may notice that their dollars stretch less far than they used to, affecting their overall quality of life.

To illustrate the impact of inflation, let us delve deeper into some key areas where families are feeling the pinch:

- Rising costs of groceries: The price of everyday items, such as milk and bread, can significantly strain your wallet. According to Statistics Canada, grocery prices have seen an alarming increase over the past year, with staples like vegetables and meat costing markedly more. For instance, by analyzing data, one can find that the price of a loaf of bread has surged, causing families to reconsider their meal plans and perhaps rely more on budget-friendly options.

- Increased utility bills: Heating and electricity costs can rise, especially during harsh winters. In provinces like Alberta and Ontario where winters can be particularly frigid, families frequently wrestle with the decision of how to keep warm while managing soaring electricity bills. Households may find themselves dialing back on their thermostat settings or exploring energy-efficient appliances that promise lower utility costs.

- Heightened interest rates: As banks adjust rates, loans and mortgages become more expensive. For many Canadians, tightening budgets mean reconsidering their housing situations. A rise in interest rates affects mortgage payments, leading families to contemplate whether to rent or buy, or even consider downsizing their living spaces just to keep up with financial demands.

With these realities in mind, many families are left wondering how to adapt their finances. Adjusting your budgeting strategies can be crucial to stay afloat during these volatile economic times. This may involve reassessing monthly expenditures, cutting back on non-essential purchases, or seeking out local farmers’ markets to find fresh produce at more reasonable prices.

In this article, we will explore practical tips for adjusting your family budget in response to inflation. Simple adjustments can make a significant difference; for instance, utilizing budgeting apps can help track spending habits more effectively or setting up automatic savings can ensure that funds are allocated for future needs despite rising costs. By taking proactive steps, you can preserve your family’s well-being and minimize the emotional stress that accompanies financial uncertainty. Implementing these strategies can lay the groundwork for improved financial stability, allowing families to feel more secure amidst economic fluctuations.

DISCOVER MORE: Click here for essential tips

Strategies for Adjusting Your Family Budget

In today’s economic landscape, where inflation continually affects household budgets, it’s essential for families to develop a more strategic approach to managing their finances. The key lies in understanding spending habits, identifying areas for improvement, and implementing practical changes that promote financial stability. By making informed choices, families can meet their essential needs while easing the strain of rising costs.

Create a Detailed Budget

One of the most effective tools for financial management is a detailed budget. Start by cataloging all sources of income, including salaries, freelance work, and rental income, if applicable. Next, break down expenses into essential categories, such as housing costs (mortgage or rent), utilities (electricity, water, gas), and groceries. This categorization helps paint a clear picture of where your money is going. In contrast, non-essentials could cover areas like dining out, entertainment, and vacations. Utilizing budgeting apps or spreadsheets can further simplify this process, enabling families to track their finances seamlessly.

Identify Necessities vs. Luxuries

As families become more budget-conscious, it’s crucial to distinguish between necessities and luxuries. Take the time to evaluate various subscriptions and memberships—such as streaming services, gyms, and magazine subscriptions—that may not be used frequently. For instance, a family might reconsider their monthly dining habits by replacing restaurant visits with home-cooked meals, introducing weekly family cooking nights that not only save money but also promote togetherness. These little shifts can create significant savings over time while still allowing families to enjoy quality moments together.

Shop Smart

Mindful shopping is an effective way to combat inflation’s impact on everyday expenses. Consider local stores and farmers’ markets for fresh produce and meats, typically offered at lower prices and in more generous quantities than chain supermarkets. Make a habit of buying items in bulk—non-perishable goods, for example—can drastically lower grocery bills. Utilizing coupons, seeking out sales, and joining rewards programs offered by local retailers can provide additional financial relief. Many Canadian grocery stores run loyalty programs, allowing families to earn points that can lead to discounts or free products, making this a smart shopping strategy.

Evaluate Transportation Costs

Transportation costs can significantly impact a family’s budget, especially with fluctuating fuel prices. It’s wise to regularly assess how these costs can be minimized. Consider carpooling to work or school, which can lessen the burden of fuel expenses while fostering community relationships. Additionally, using public transport or combining errands into a single trip not only saves on gas but also reduces wear and tear on vehicles. For shorter distances, consider walking or biking; not only will you save money, but you’ll also engage in healthier lifestyles while enjoying the outdoors.

Adjusting your family budget is not merely about tightening the purse strings; it requires a proactive mindset and the ability to adapt. Raising financial awareness within the family by openly discussing spending habits and long-term goals fosters an environment of transparency and responsibility. This collaborative approach can help prepare children for future financial challenges, instilling a sense of financial literacy and independence early on.

Ultimately, making small adjustments, such as re-evaluating subscriptions or changing shopping habits, can yield significant benefits and enhance your family’s resilience to financial pressures. As you navigate these strategies, remember that each step you take toward fiscal prudence contributes to a more secure future, allowing families to better weather the storms of economic uncertainty.

DISCOVER MORE: Click here to learn about investment diversification strategies

Additional Strategies for Financial Resilience

As families navigate the ever-changing waters of inflation, it is crucial to adopt a multifaceted approach to sustaining their financial health. Beyond traditional budgeting and shopping strategies, families can explore various resources and techniques that can further alleviate financial stress while fostering a culture of financial acumen within the household.

Automate Savings

One effective method to build a financial cushion is to automate savings. Setting up automatic transfers to a dedicated savings account right after payday ensures that families prioritize savings before discretionary spending. This “pay yourself first” mentality can significantly enhance financial stability over time. By creating an emergency fund that can cover three to six months of expenses, families can insulate themselves against unforeseen costs that inflation may bring, such as unexpected medical bills or home repairs.

Consider Side Hustles

In today’s gig economy, families can consider starting a side hustle to supplement their income. Many Canadians have turned hobbies into money-making ventures, whether it be freelance graphic design, online tutoring, or selling homemade crafts on platforms like Etsy. Beyond offering extra revenue, side hustles can also cultivate new skills and provide a sense of accomplishment. Moreover, leveraging platforms such as Skillshare or Udemy can broaden one’s professional capabilities, making future career transitions smoother and more profitable.

Revisit Your Insurance Policies

In turbulent economic times, it’s wise to review and compare insurance policies. Many families may be overpaying for insurance coverage that no longer suits their needs. Regularly assessing home, auto, and health insurance policies offers the chance to identify better rates or coverage options that can save money. Engaging with an independent insurance broker can provide insights into competitive options tailored to your family’s specific situation, ensuring that you aren’t leaving money on the table.

Take Advantage of Government Programs and Tax Credits

Another avenue families can explore is the assistance and tax credits offered by the Canadian government. From the Canada Child Benefit (CCB) to various provincial support programs, families might be entitled to financial assistance that alleviates their budgetary constraints. Moreover, tax credits related to education, purchasing energy-efficient appliances, or childcare can result in significant savings that directly impact your bottom line. Understanding what is available and ensuring you are making the most of these offerings can have a profound effect on overall financial health.

Invest in Financial Literacy

Families should also consider the long-term benefits of investing in financial literacy. There are numerous resources available, from online courses to community workshops, focusing on budgeting, investing, and debt management. Understanding how money works, including interest rates, inflation, and the stock market, can empower families to make educated decisions that bolster their financial future. Encouraging children to engage in these discussions nurtures a financially savvy generation that is better equipped to face economic challenges.

By implementing these additional strategies, families can strengthen their financial resilience amid inflationary pressures. Each small step taken helps to enhance not only the stability of the family budget but also fosters a deeper understanding of money management principles that can benefit future generations.

LEARN MORE: Click here for details

Understanding Financial Adaptability

In today’s economic climate, where inflation feels like an unwavering presence, the ability to adapt one’s financial strategies is crucial for families across Canada. As the cost of living rises—impacting everything from groceries to housing—families must take a proactive stance to manage their finances in a meaningful way. Achieving financial stability demands not just awareness but a commitment to change and innovation in financial practices.

One effective strategy is automating savings. By setting up automatic transfers to a savings account each month, families can ensure that they consistently put money aside without the temptation to spend it. This technique allows individuals to treat savings as a non-negotiable expense, akin to paying bills. For instance, if a family allocates $200 a month into a high-interest savings account, they’ll benefit from compound interest, leading to significant savings over the years.

Additionally, exploring side hustles has gained popularity among Canadian families aiming to create additional streams of income. Options such as freelance work, online tutoring, or starting an Etsy shop can provide flexibility in hours and allow families to earn extra money while managing their time effectively. For example, a parent could leverage their expertise in graphic design while still caring for their children during the day, thereby contributing financially without sacrificing family time.

Leveraging Resources

Furthermore, regular reviews of insurance policies are essential in this era of economic uncertainty. Families should assess their coverage to identify potential savings and ensure they are not overpaying for unnecessary features. In many cases, switching providers or negotiating renewals can lead to considerable savings. Canadian families should also explore government programs and tax credits. Financial assistance programs, such as the Canada Child Benefit, can provide critical support that makes a difference in monthly budgets.

Investing in financial literacy forms the foundation for making informed decisions. By engaging in workshops or accessing online resources, families can learn to navigate their finances better. Programs offered by local libraries or community centers often provide valuable information tailored to Canadian families, helping build resilience and cultivate a mindset geared towards long-term financial health.

Small Changes, Big Impact

Remember, it is often the small, strategic adjustments that yield significant benefits over time. When families integrate a culture of financial awareness into their daily lives, they equip themselves to withstand inflation’s challenges while setting the stage for a prosperous future. By embracing automated savings, exploring new income avenues, regularly assessing their insurance, and educating themselves about financial resources, Canadian families can stay ahead of economic fluctuations.

Ultimately, fostering financial adaptability is a powerful tool that ensures families are not merely surviving amidst inflation but are also thriving, regardless of what the future holds. With the right mindset and a commitment to proactive financial management, families can navigate the complexities of today’s economy and build a solid foundation for generations to come.

Linda Carter

Linda Carter is a writer and financial expert specializing in personal finance and financial planning. With extensive experience helping individuals achieve financial stability and make informed decisions, Linda shares her knowledge on our platform. Her goal is to empower readers with practical advice and strategies for financial success.